You’re getting refunds and offers—then the bill hits

It usually starts looking better than expected. The bursar email says a refund is on the way, your card app flashes a “0% for 15 months” offer, and the paycheck from a campus job finally lands on a steady cadence. For a week or two, the account balance holds, and it feels like the semester’s costs are already handled. Then a lab fee posts late, the insurance waiver doesn’t apply, or the bookstore charge clears after the drop deadline. The timing is the trap: money arrives once, bills arrive whenever they feel like it.

In practice, the refund is just a routing event, not a cushion. If it’s spent before the semester’s full set of charges has actually settled, the gap gets covered by whatever is fastest—usually a credit card. The card doesn’t complain until the statement closes, and that silence is what makes the hit feel sudden.

The constraint is simple and brutal: due dates don’t care that your aid and paychecks came early. When the bill finally shows the real number, the “extra” money has already been assigned to groceries, a trip, or a laptop payment plan.

Treating the refund like income backfires fast

The move that creates the mess is subtle: the refund gets mentally renamed as “what I can spend,” instead of “what I’ll need to survive the gaps.” It’s easy to do when the deposit is larger than any single bill you’ve seen so far. A laptop upgrade feels reasonable. Booking spring break early feels efficient. Even paying down a card can feel like progress. But the refund isn’t new income; it’s borrowed money that already has a job, and interest starts running the moment school disburses it.

Once it’s treated like a bonus, the next month turns into substitutions. Food goes on the card because cash is thinner than expected. A rent shortfall becomes a balance transfer. Minimum payments start competing with textbooks. The constraint isn’t discipline—it’s that the refund was supposed to cover uneven weeks, and now the card is covering them at 20%+ APR.

The fastest fix is boring: park the refund in a separate account and “pay yourself” weekly. If it still feels like extra after census date and all fees settle, then it’s actually extra.

The budget fails when dates don’t match reality

That weekly “pay yourself” plan looks clean on paper until the calendar starts misbehaving. Rent wants the 1st, the card statement cuts on the 17th, your paycheck hits Fridays, and financial aid won’t disburse again for months. A budget built on monthly totals can still fail if the cash isn’t in the account on the day the charge clears. The mistake isn’t overspending; it’s assuming timing will average out before fees show up.

The tell is how often you’re forced into workarounds: moving due dates, floating a bill for “just a few days,” or letting autopay hit while you manually transfer money to cover it. Each patch adds friction and increases the odds of a $35 overdraft or a late fee that blows up the week’s food money.

The fix is to budget by pay cycle and due date, not by category. Map the next 30 days of actual withdrawals, then hold a small “timing buffer” so one delayed deposit doesn’t turn into revolving debt.

Credit card points aren’t worth a damaged score

Once the timing buffer is thin, points start looking like a workaround. The card offers 3% back on dining, a sign-up bonus that could cover a flight, and an app that makes “utilization” feel abstract. But the credit bureaus don’t care why the balance rose. If a $1,000 limit card sits at $700 while you wait for a paycheck, you’re signaling stress even if you plan to pay it off.

The constraint is that scoring reacts to what’s reported on the statement date, not what you do a week later. People chase rewards by pushing spend onto the card, then get surprised when a new apartment application or post-grad car insurance quote comes back worse than expected. A 30-day late payment is even harsher—it can stick for years, and the points earned that month are basically irrelevant.

The cleaner trade is to treat points as a bonus only when the balance is already easy: autopay the statement balance, keep reported utilization low, and ignore rewards that require spending you wouldn’t do in cash.

Small subscriptions quietly erase your food budget

After you stop chasing points, the leaks get quieter. The charges aren’t “shopping,” so they don’t trigger the same guilt—$5.99 here, $12.99 there, a cloud plan, a gym add-on you meant to cancel after midterms. The constraint is timing again: most of these hit on random days, and they hit whether or not your paycheck cleared or your refund is still sitting in a separate account.

What makes subscriptions brutal on a student budget is how they stack against the one category that has to flex: groceries. A $45 bundle of “small” autopays can be two decent trips to the store, and it usually lands right before a weekend when food spending spikes. If you’re trying to keep a card balance low for credit reasons, those autopays also force you to choose between utilization and eating well.

The fix isn’t to become a minimalist; it’s to make them compete. Put every subscription on one list, total it, and cap it like rent—then cancel anything that doesn’t earn its spot every month.

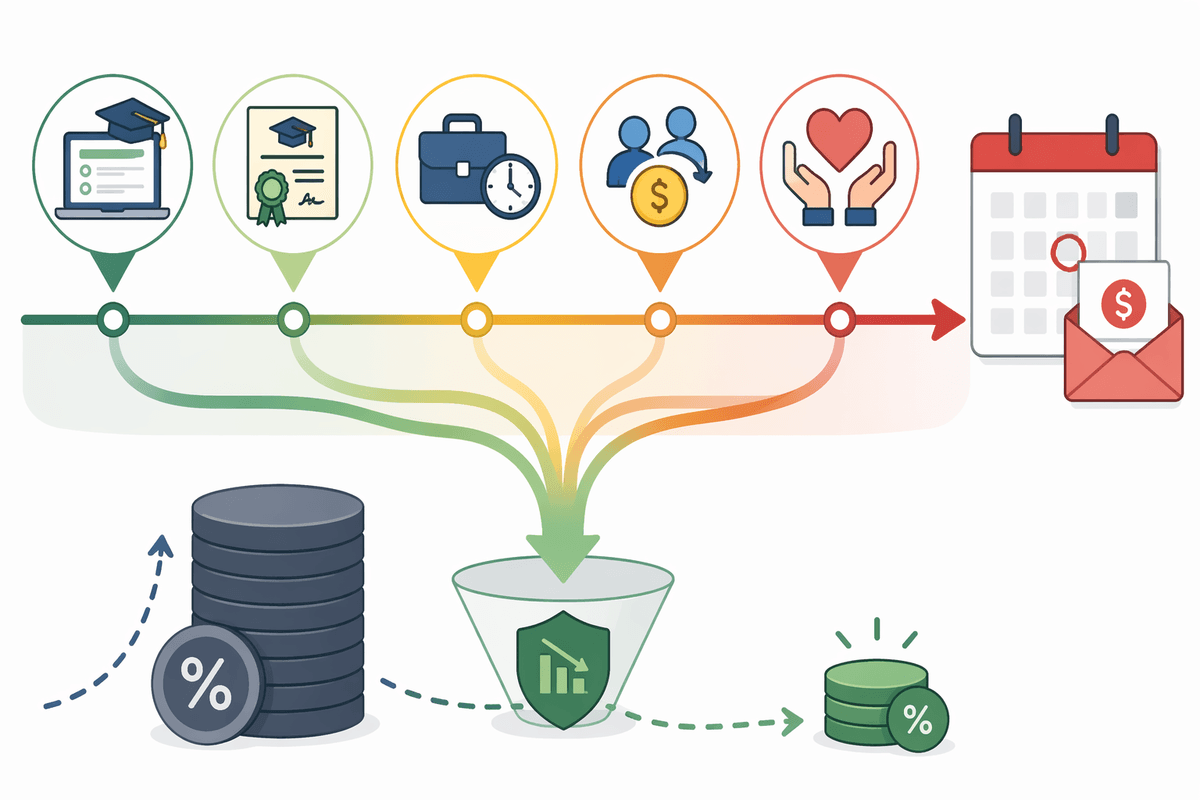

Ignoring free money makes debt feel inevitable

After subscriptions are capped, the monthly numbers finally look less cruel, but the account can still feel pinned down. That’s usually when people resign themselves to, “I’ll just carry a balance until I’m working full-time,” even though some cash is sitting on the table. The friction is that free money doesn’t arrive automatically: it’s hidden behind forms, deadlines, and portals that don’t sync with school life. When you’re busy, it’s easier to pay interest than to log in and chase $200.

The common misses are boring and expensive: not filing FAFSA early enough for priority aid, skipping work-study because it sounds inconvenient, ignoring employer 401(k) matches at a campus job, or leaving scholarship renewals unfinished. Even credit card interest waivers, fee reversals, and hardship plans can exist, but only after you ask. The constraint is timing—most of these require action weeks before the bill is due.

A good rule is to schedule one “free money hour” per month: check the financial aid portal, search your department’s scholarships, confirm work-study eligibility, and review any match or benefit at your job. The debt stops feeling automatic when the system starts paying you back on purpose.

Graduating ahead is mostly systems, not willpower

By late spring, the difference between “I’m barely making it” and “I’m weirdly okay” isn’t motivation—it’s whether the defaults are doing the work. The week after finals is when a lot of people loosen the structure: refunds are gone, hours shift, and the card becomes the bridge again. The constraint is time: once graduation paperwork and job hunting stack up, even small money tasks get skipped, and the fees return.

The setups that actually hold are plain. One account for bills, one for spending, and an automatic transfer every payday that funds next month’s fixed costs first. Autopay minimums to avoid lates, plus a separate scheduled extra payment to kill the highest APR balance. If income bumps after graduation, the system captures it before lifestyle does, and the “ahead” feeling sticks.